Please note: The due date for Financial Bank and Financial Accounts FBAR Filing for financial accounts maintained during calendar year 2016 is April 18, 2017, consistent with the Federal income tax due date.

This date change was mandated by the Surface Transportation and Veterans Health Care Choice Improvement Act of 2015. The Act also mandates a maximum six month extension of the filing deadline.

To implement the statute with minimal burden to the public, filers failing to meet FBAR annual due date of April 18th, will grant an automatic extension to October 15th.

Who Must File an FBAR

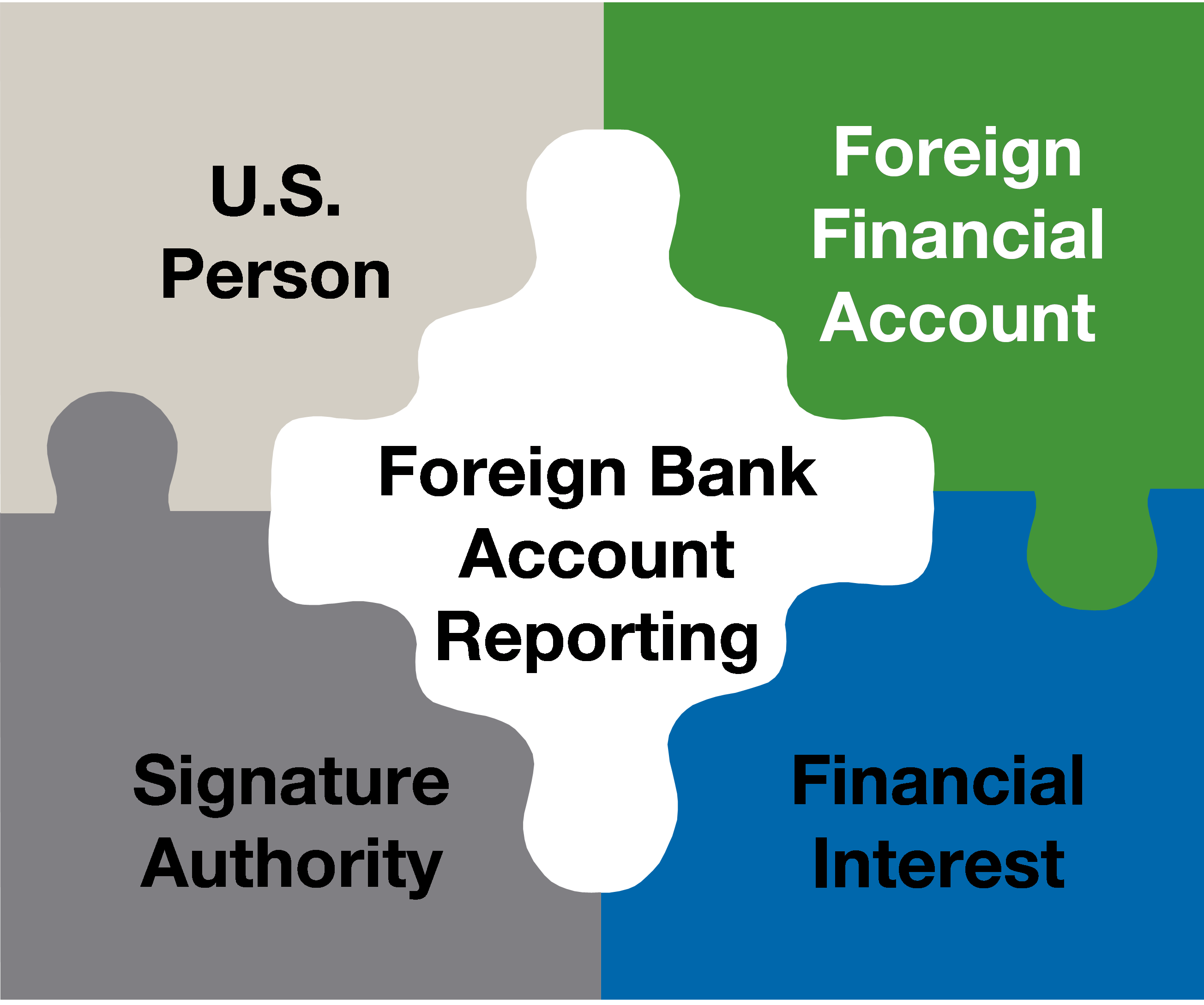

United States persons are required to file an FBAR if:

1. the United States person had a financial interest in or signature authority over at least one financial account located outside of the United States; and

2. the aggregate value of all foreign financial accounts exceeded $10,000 at any time during the calendar year reported.

United States person includes U.S. citizens; U.S. residents; entities, including but not limited to, corporations, partnerships, or limited liability companies, created or organized in the United States or under the laws of the United States; and trusts or estates formed under the laws of the United States.

A person who holds a foreign financial account may have a reporting obligation even when the account produces no taxable income.

FBAR Penalties

Those required to file an FBAR who fail to properly file a complete and correct FBAR may be subject to a civil penalty not to exceed $10,000 per violation for non willful violations that are not due to reasonable cause. For willful violations, the penalty may be the greater of $100,000 or 50 percent of the balance in the account at the time of the violation, for each violation.